Just the other day, I saw a news article that raised the question of whether utilities' sales are trending up. Considering the reports from EIA and other agencies indicating flat sales, the headline caught my attention. As a forecaster who helps utilities peer into the future, I am very interested in other opinions – especially ones that challenge my assumptions.

The article cites two large utilities with 2013 weather normalized sales growth rates of 1.6% and 1.7%. While the article was fair in raising the question and not asserting a new trend in electric sales, anyone reading the article would and should pause to consider the author’s assumptions. My theories are based on our annual surveys and discussions within the industry. Itron’s two recent surveys show weighted average normalized energy sales growth of 0.22% and 0.33% in 2012 and 2013 respectively.

So, do the 1.6% and 1.7% numbers indicate a change in trend? How do I reconcile those numbers with my assumptions? I decided to investigate quickly.

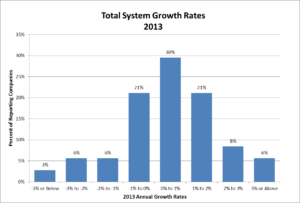

While the 2014 Itron survey results show an average growth rate for 2013 of 0.33%, is it uncommon for a utility to show a 1.7% growth rate? Instead of looking at the average, I built a distribution of the reported growth rates as shown below.

The distribution shows that 30% of the 71 respondents have 2013 growth rates between 0% and 1%. However, 21% claim growth between 1% and 2%. In fact, 1.7% is within a standard deviation of the 0.3% mean. With the article's stated sample size of two utilities, their growth rates are well within the range of possible results.

I certainly do not fault the article for citing only two utility numbers. These growth rates are difficult to obtain and we spend a significant amount of time working on the benchmarking survey. Hopefully, the annual surveys are valuable to you (our customers) and you continue to actively participate in them.

But, the lessons are clear to all of us forecasters:

(1) one number does not make a trend,

(2) every utility is different, and

(3) sales growth rates are a hot topic within our industry.

And, it’s always good to challenge our assumptions.

Mark Quan is a Principal Forecast Consultant with Itron’s Forecasting Division. Since joining Itron in 1997, Quan has specialized in both short-term and long-term energy forecasting solutions as well as load research projects. Quan has developed and implemented several automated forecasting systems to predict next day system demand, load profiles, and retail consumption for companies throughout the United States and Canada. Short-term forecasting solutions include systems for the Midwest Independent System Operator (MISO) and the California Independent System Operator (CAISO). Long-term forecasting solutions include developing and supporting the long-term forecasts of sales and customers for clients such as Dairyland Power and Omaha Public Power District. These forecasts include end-use information and demand-side management impacts in an econometric framework. Finally, Quan has been involved in implementing Load Research systems such as at Snohomish PUD. Prior to joining Itron, Quan worked in the gas, electric, and corporate functions at Pacific Gas and Electric Company (PG&E), where he was involved in industry restructuring, electric planning, and natural gas planning. Quan received an M.S. in Operations Research from Stanford University and a B.S. in Applied Mathematics from the University of California at Los Angeles.